Why not REDUCE (or eliminate) corporate taxes?

HB 322 is being heard this morning (Wednesday the 22nd) in House Tax Committee. The bill does two things: It creates a single corporate income tax rate of 5.9 percent and requires all business income to be apportioned by the single sales factor. Currently, there are two corporate income tax rates with 4.8% which applies to corporations with profits below $500 thousand (and larger businesses on their first $500,000 in profits).

The factor of taxation has mixed implications for different industries, but overall, this is a tax increase. The FIR is for $7 million annually.

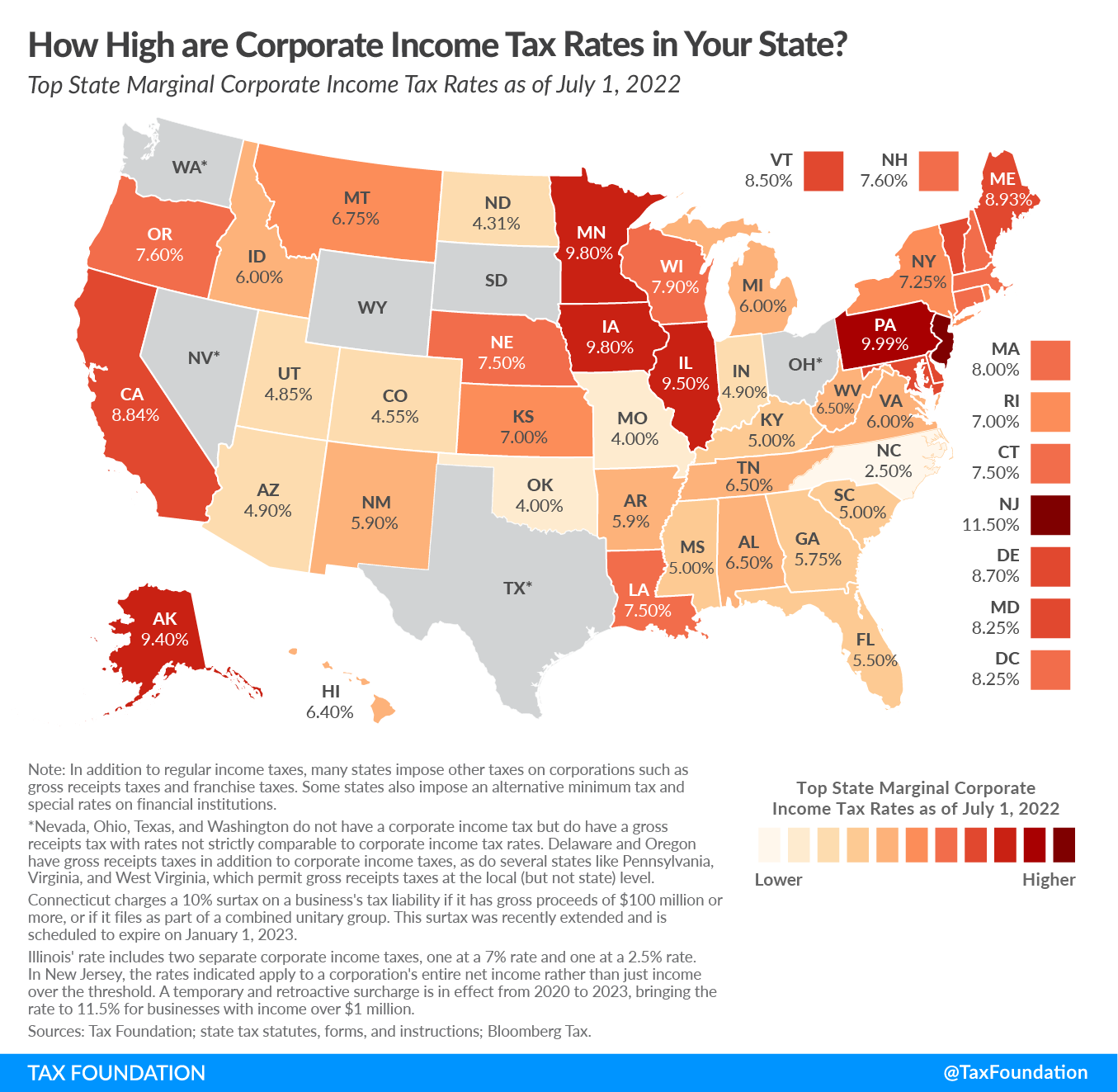

With all the talk of economic diversification and the massive budget surplus available to the Legislature, New Mexico should be looking to eliminate entirely, not raise or even mildly alter our corporate income tax. In recent years revenues from the tax have hovered between $300 and $400 million annually.

As is usually the case when it comes to taxes, New Mexico’s rate is higher than that of any of its neighbors.