Schardin Clark is missing the boat on New Mexico’s income tax

08.06.2026

Recently, Stephanie Schardin Clarke, New Mexico Secretary of Taxation and Revenue, wrote an article slamming Republican efforts to eliminate New Mexico’s personal income tax. She makes numerous points, but they boil down to two: 1) We simply should not cut taxes, especially for the wealthy. 2) New Mexico cannot afford to do bold things to improve its economy and instead must be content to “smaller” policies like targeted tax credits.

Schardin Clark touts small, targeted policies that have been implemented over the past eight years but fails to note that the only thing truly propping up New Mexico’s economy is the ongoing oil and gas boom in the Permian Basin. That money has contributed to 75% spending growth under the current Administration, not to mention new entitlements like “free” college, “free” universal childcare, and “free” universal pre-K that will continue to drive spending in the future with questionable and unproven outcomes.

The economic impact of these programs is unknown. Spending is happening, but will these policies result in a better trained workforce, overall job creation, or anything that will make New Mexico and New Mexicans more successful? It is impossible to say.

But, in terms of Schardin Clarke’s approach to taxes, the fact is that even at a time of record oil and gas revenues, Lujan Grisham has raised taxes more than she’s cut them. Yes, reducing New Mexico’s GRT by .25% was a “win,” but she also signed an income tax hike, levied taxes on online sales, and increased corporate income taxes. Just this year the Gov. signed legislation increasing vehicle registration fees by 25%.

All of this at a time when Senate Finance Committee Chair George Muñoz (a Democrat) says “We have more money than we know what to do with.” Muñoz appears to have figured things out and recently wrote an opinion piece in support of eliminating the personal income tax.

The point is that under Lujan Grisham and Schardin Clark New Mexico has NOT seized the opportunity to truly diversify and grow its economy. They tout very narrow and short-term statistics, but ignore the fact that New Mexico remains the third-most impoverished state in the union and people are “voting with their feet” making New Mexico’s population stagnant and aging dramatically relative to our neighbors.

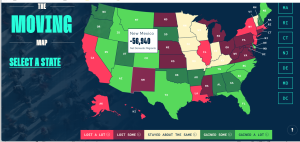

Eliminating New Mexico’s personal income tax would lead to economic growth in New Mexico and would likely stanch the outward migration of our young, educated population. In fact, “Between April 1, 2020, and June 30, 2023, high-tax states lost net 2.8 million residents to low-tax states. Zero-income tax Florida and Texas were the top two destinations for interstate movers, gaining 819,000 and 656,000 net residents respectively.” This isn’t an abstract issue.

New Mexico lost population last year according to the US Census Bureau. If you want your kids and grandkids to stay in New Mexico you need to do something big to make the State more attractive to people and business.

So, what should be done? Rather than eliminating the $2.1 billion generated by the income tax in one fell swoop, I recommend phasing out the income tax over a span of a few years. Already for the next session analysts expect no less than $850 million in “unforeseen” revenue thanks to rising oil prices. This number is likely closer to $1 billion given continued high oil prices. NO OTHER TAXES should be raised to eliminate the income tax!

So, reduce the income tax by approximately $1 billion. If revenues don’t keep up (say oil prices drop dramatically or the US goes into a recession) those tax cuts can be reversed or put on hold. There’s no need to cut necessary programs although it is true that New Mexico government is far too bloated and many of these programs (like “free” childcare and “free” pre-K) SHOULD be targeted at those with lower incomes, not the wealthy.

For too long New Mexico has relied on oil and gas and federal spending. While we shouldn’t kill off oil and gas we DO need to diversify our economy. Eliminating the income tax would do that by bringing new businesses and taxpayers to New Mexico. It is high time to do something bold to improve our state.